Climate change is receiving increasing attention. In the Netherlands, homes are at risk from flooding as a result of heavy rainfall.

But what is the risk for an individual residential property in a flood zone when purchasing?

Risks in the future

Risk=Chance×Damage

This means that both the probability of a certain type of damage and the associated costs must be known to calculate the risk.

However, the damage will only become apparent sometime in the future. This means that depreciation, or the devaluation of money, must be taken into account. After all, a euro in the future is worth less than a euro today.

The depreciation of money can be calculated using the Net Present Value Method. This method uses a discount rate, which indicates how much the required money could have yielded if it had been used differently. For example, by opening an investment account.

An example

Suppose a residential property is purchased for €450,000, with a 30-year mortgage. The property has three risks of water damage that are not reflected in the price:

- Minor problems

Average cost of €500 once every three years for:

-

- Moisture spots and mud residue on walls and floors

- Damaged stucco and paint due to brief immersion

- Medium problems

On average, once every 5 years, €5,000 in costs for:

-

- Moisture in floors and walls leading to warping of laminate or parquet flooring

- Windows and doors that close poorly due to slight deformation

- Minor electrical faults (sockets, switches)

- Major problems

On average once every 25 years €20,000 in costs for:

-

- Wide cracks in masonry due to saturation of the substrate

- Damaged wooden beams and window frames due to prolonged immersion

- Electrical installations and pipes that need to be completely replaced

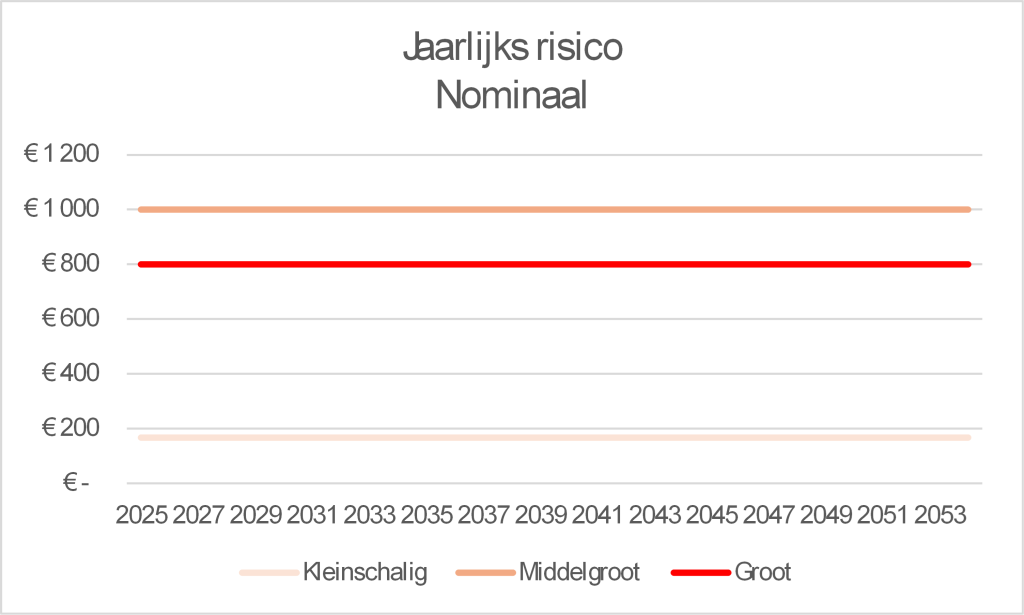

The annual risk for minor problems is €167 (= 33.33% x €500). The annual risk for medium-sized problems is €1,000 (= 20% x €5,000) and the annual risk for major problems is €800 (= 4% x €20,000).

If the depreciation of money were not taken into account, the risk for the next 30 years would be €59,000: €5,000 for minor problems, €30,000 for medium-sized problems, and €24,000 for major problems.

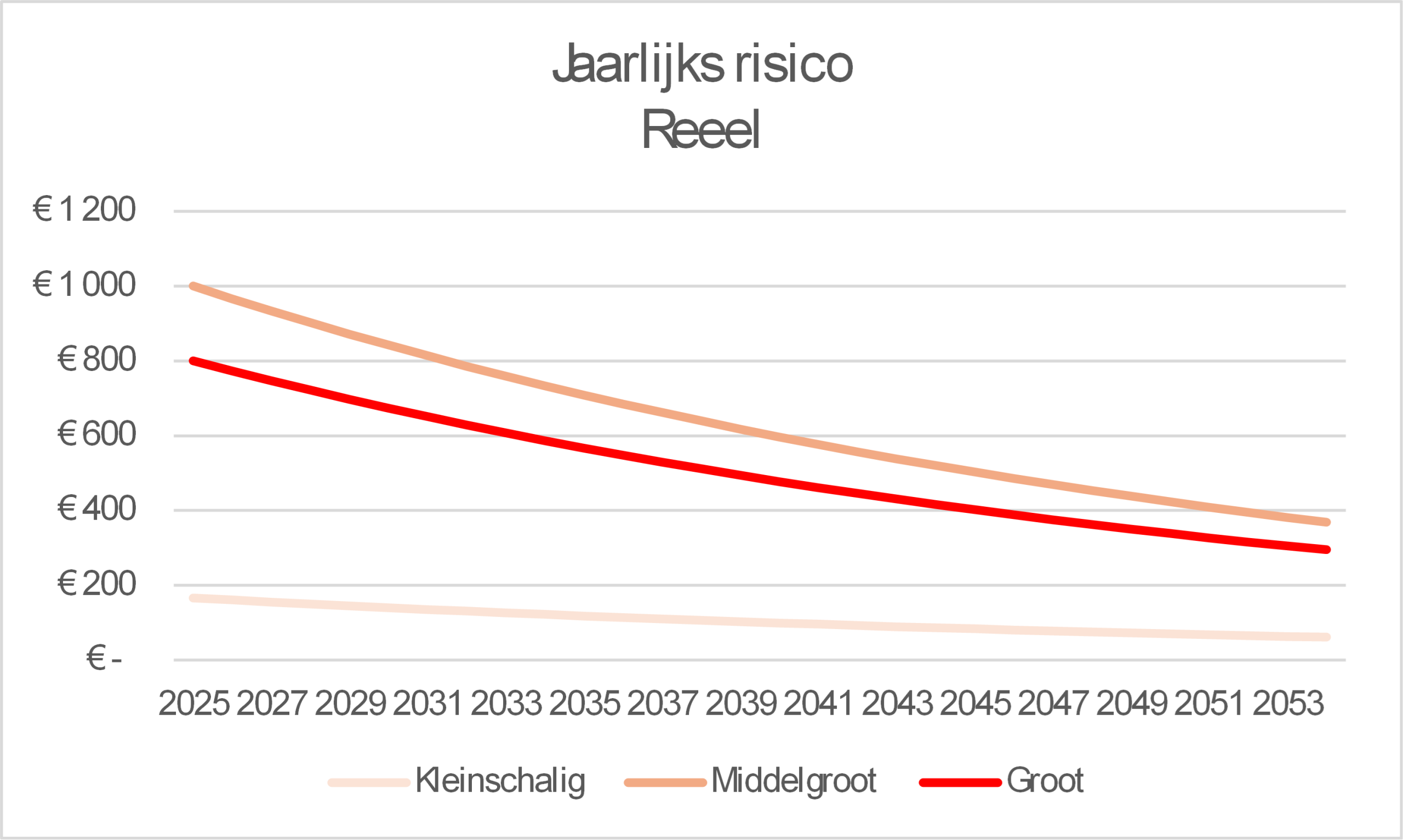

Taking into account a discount rate of 3.5%, the annual risks are as follows:

The total risk is then equal to €37,437.

Climate change is leading to more extreme weather, increasing the likelihood of more serious problems causing much greater damage, including the total loss of a home. By accurately assessing the increasing likelihood of total loss, the risk can be estimated.