In general, risk means that there is a chance of an unfavorable event occurring or the danger that something will go wrong. If you want to express a particular risk in euros, the formula is as follows:

Risk=Chance×Damage

The risk associated with a mortgage loan depends, among other things, on the borrower’s creditworthiness and the financing conditions, but also on the likelihood that the collateral will yield less than the mortgage when sold.

Value of the collateral relative to the mortgage loan

To determine the risk that the collateral will yield too little upon sale, the probability distribution of its value is necessary. Only in this way can the probability be determined that the value will be lower than the mortgage.

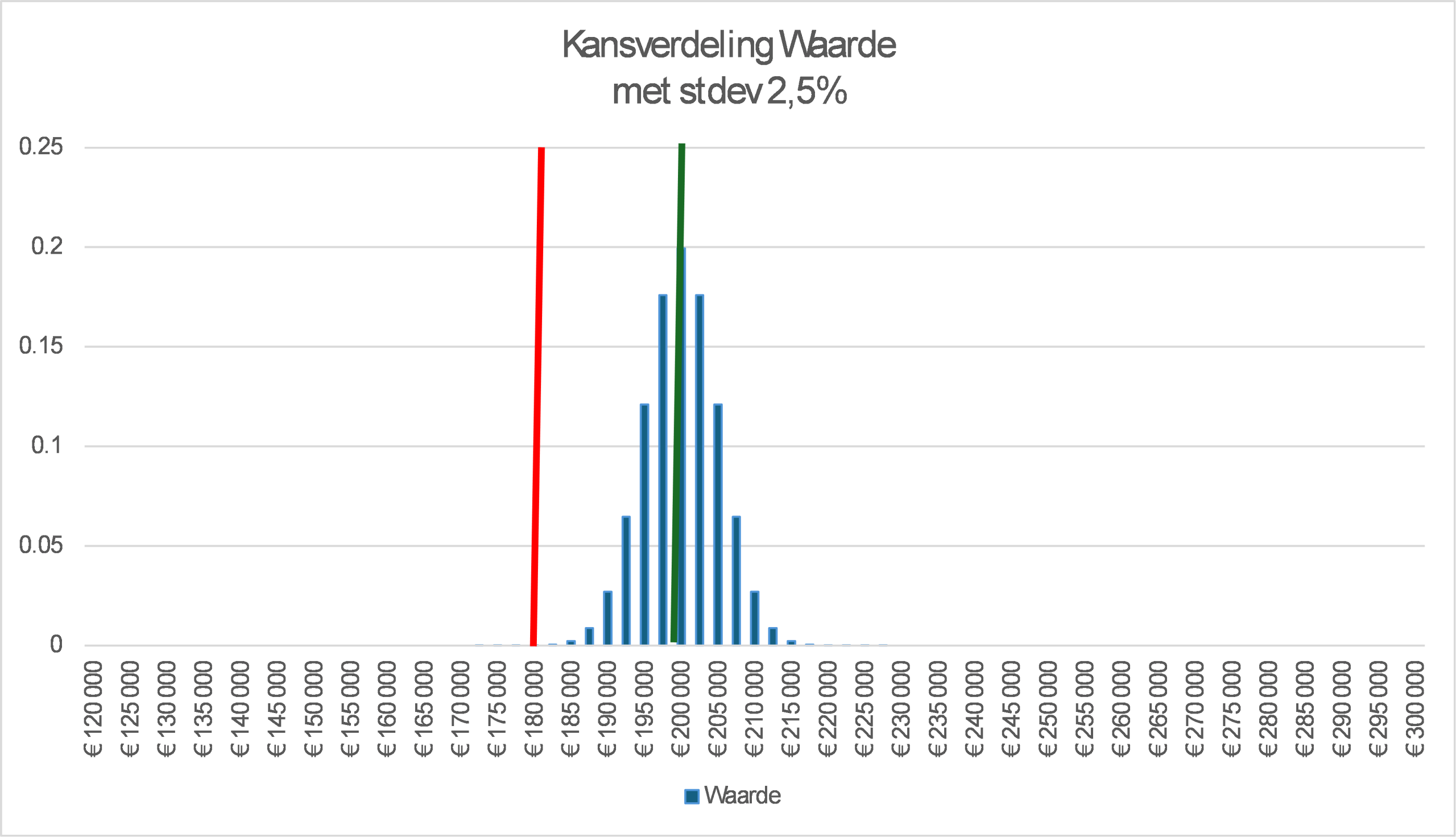

For example: The value of a home is €200,000 and has a probability distribution with a standard deviation of 7.5%. The mortgage is equal to €180,000.

The probability that the value will be lower than the mortgage is equal to the sum of all blue bars to the left of the red line, which amounts to 7.8%.

The probability that the house will be sold for, say, €175,000 is equal to the length of the corresponding bar, approximately 0.016%.

In that case, the loss would be equal to €175,000 – €180,000 = €5,000.

The risk associated with a sale price of €175,000 is equal to €80 (0.016 x €5,000).

The probability that the sale price will fall below the amount of the mortgage can be determined by performing this calculation for all bars to the left of the red line and adding up the results. This leads to €8,075.

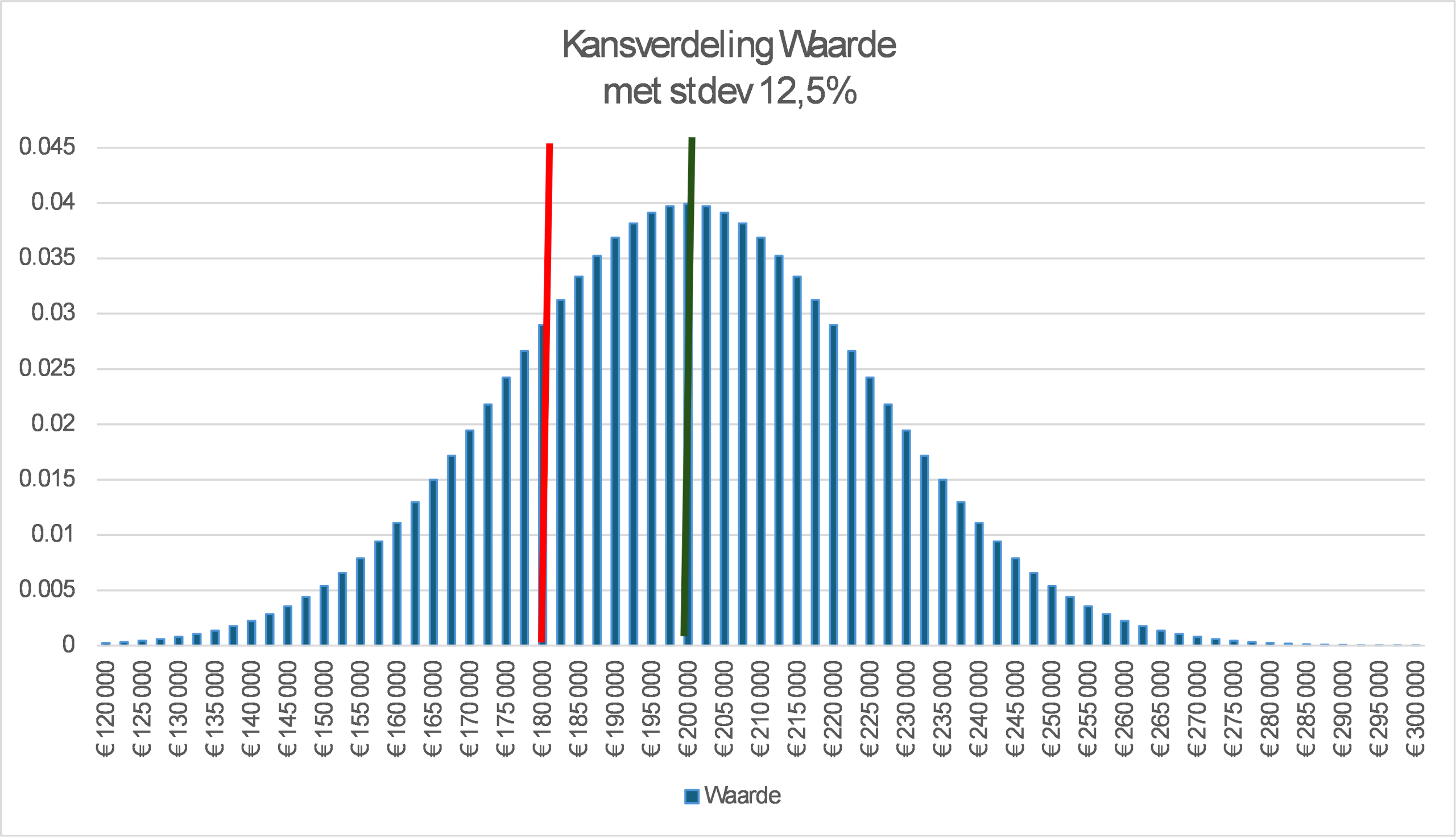

Importance of a good valuation

The certainty of the valuation is reflected in the probability distribution of the value. The narrower the distribution, the higher the bars around the average and the more certain the valuation. (The standard deviation is used as a measure for this).

For example, if the standard deviation were equal to 2.5%, the graph would look like this: